Renko options trading strategies are effective for QQQ position trading and for generating income. When position trading, you can use the Renko method, trading options positions instead of the actual QQQ. And for options income, you can sell puts and calls either uncovered or in credit spreads.

So, if your trading account size was big enough, you could Renko position trade the QQQ; 200 shares would cost around $74,00 without using margin. However, Renko options trading will allow you to trade the same basic positions with far less cost. If you use QQQ synthetic options positions, your cost can be close to zero.

And you can also use QQQ options to hedge positions in order to hold them longer term with the larger price swings.

Renko options trading combinations give you the flexibility that underlying trades alone cannot provide. For example, QQQ option income and position hedges are things you cannot do through underlying trading.

Renko QQQ Position Trading For The Underlying

If you look at the chart below, you may think you’re looking at a day trading chart with all the yellow circles on it. However, this is a Renko position trading chart of the QQQ with a brick setting of one point.

Even with all of the yellow circles, there still is not more than one trade in a day. The trades don’t include an initial trade with an add-on trade.

Since this is QQQ position trading, we prefer that there were multiple days between trades, similar to the large downswing on the left side of the chart. But this was the situation where, after the low and a retracement back to resistance, the QQQ compressed inside the triangle you can see on the chart.

Before discussing Renko option trading for both price direction and income, let’s review the chart as if the QQQ underlying was what you traded.

Renko Chart Strategies: Renko Indicators, Patterns, Trade Filters

Renko Chart QQQ Position Trading

Yellow circles 1-2: A price envelope reverse follows these, and then a midline reject add-on occurs. This is what I mean by trading price direction. These are the initial Renko trade setups for a swing reverse. The trades continued to price resistance and would be profitable since they moved at least four bricks.

Even though this is Renko position trading, we still use our base method indicators and trade setups. The trades discussed are a good example of what I mean.

Yellow circles 3-4: After resistance hits, you can see the momentum extreme, and a new swing follows. This time, we got a price envelope reverse and midline reject short trades. When you use the Renko method, a 4-brick move against them stops you out of your trade.

Pink circle1: Here’s another price envelope reverse, but you can’t make this trade. The setup filters for the resistance price and MEx hasn’t crossed.

QQQ Position Trade Quantity

A further look at the times for these trades:

- Yellow circles 1-2 were on 9-27 and 9-28, so even the add-on wasn’t on the same day as the initial trade.

- Yellow circles 3-4 were on 9-29, and you stopped out on 10-2 along with the pink circle.

- And then the next trade was on 10-3.

So again, there is more trading activity than I would like for Renko position trading, but still, fewer trades than we would have with day trading.

Yellow circles 5-6: price envelope reverse sell, followed by a price envelope reverse buy. But as you can see, MEx is still down, and you filter the trade for the downtrend line. You hold the sell, and another price envelope reverse and swing resumption follows. That becomes an add-on short since you held the initial trade. The price moved over 4 bricks so that these trades would be profitable.

Pink circles 2-3-4: the price higher low gave us the uptrend line to form the triangle pattern. The pink circles were all trades inside the triangle that you wouldn’t made because of filtering for the trendlines.

Yellow circle 7: The Renko trade shows a triangle breakout synched with the price envelope reverse buy. You can see the breakout moved the price back to resistance and continued through, again giving us a profitable move of over four bricks.

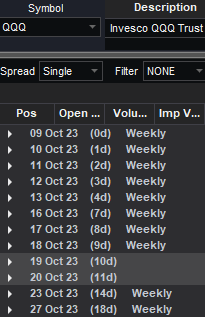

Options Expiration Dates

The section of QQQ options dates for October shows how much flexibility we have with our Renko options trading. There are weekly options with expiration dates for each day besides the monthly expiration date.

For instance, what if we use a nearer option when we buy options? And then, when we sell options, we go farther out?

If we could use that Renko options trading strategy, the options we buy would cost less than the premiums we received for the options we sold.

Look at the chart below and see how these strategies could work.

Option Expirations Dates

There is a tradeoff to buying closer expirations for Renko option trading. On the one hand, the cost of the option will be less; however, the option might expire before the swing reverses.

An expiration of 1 week would be long enough for most of the larger swing lengths. However, the sell swing on the left side of the chart went short 9-15, and the buy reverse was 9-27 or 8 trading days.

- Do you buy expirations of 2 weeks to protect against early expiration?

- Or do you buy expirations of 1 week, anticipating that the lower option price will cover the missed profit?

There is a price envelope reverse long on 9-27, and you buy 358 calls. What expiration?

The biggest option expiration problem is when you have a Friday trade. In that case, you only cover your trade for 5 trading days with a weekly, so buy a 2-week expiration. Especially do this if you are using the long call to protect a Renko option income trade.

With a 9-27 trade date on a Wednesday, you buy 10-6 calls. This expiration will cover 7 trading days. Interestingly, if the 9-15 put buy expired 9-26 after 7 trading days, the profit would have been greater than holding until the 9-27 buy reverse.

Renko Option Trading For Income

When Renko option trading for income, you sell options. Sell an uncovered option or a credit spread. A credit spread is when you sell one option and buy another, where the short option is closer to the money than the long option.

Amongst my Renko option trading, I have been selling SPY and QQQ option credit spreads for years to generate income. I want to time the option sells for market extremes and at prices above recent highs or lows.

For instance, I am currently short SPY Oct 460-465 and Nov 465-470 for a credit of $1.60. I would also like to sell credit spreads with puts, but they are harder to fill.

Why? Because puts that are out of the money have higher implied volatility than those closer to the money, making credit for selling puts spreads tighter.

But I can sell uncovered puts, meaning they are not part of a spread. I could also sell uncovered calls and receive a far bigger credit, but I am fine with the spread for this options strategy and not using up the necessary margin. Additionally, I can have short calls as part of a Renko option trading synthetic short.

Before trading any options strategy that includes selling uncovered options, be sure you understand the risks of short options.

The chart below shows a recent trade of a Nov 320 put for 4.55 and its breakeven point. I am using a chart with the following:

- 50 and 200-day moving average

- 3 average true range Keltner channel

- RSI

The timing of the trade was the hit of the bottom channel line, and the RSI was very near oversold. You can see the room below the lower Keltner channel and the 200-day moving average to the put option income trade breakeven.

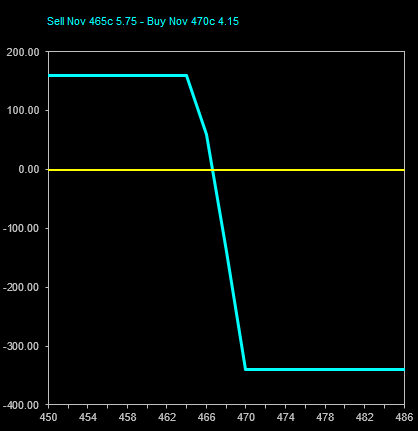

Options Call Credit Spread Risk-Reward

You are looking at the profit graph for the Nov 465-470 credit spread. The maximum gain is 1.60, with a maximum loss of 3.40. The options income credit spreads do not appear to have good risk-reward. But you know the most you can lose, and you can protect these with the Renko Options SPY position trades.

I did the trade when the SPY was around 453, and the 52-week high was 459.44.

With a breakeven of 466.60, the SPY would have to go up over 16 points and make a new high by over 7 points. And this would have to happen without you being long a Renko SPY position trade at that time for protection.

So, what these options income credit spreads give up in risk-reward, they make up in their odds of being successful trades.

Renko Options Trading Combinations

The Renko QQQ position trading chart below shows a series of trades I want to discuss. You know from the QQQ position trading chart above that more trades occurred than marked on this chart. I want to focus on the flexibility of Renko options strategies and creating positions using existing trades.

View Renko options trading as a combination of positions instead of individual trades:

- An income trade can become part of a directional synthetic long by combining it with a long option.

- A directional option trade can protect an income trade by creating a long debit spread.

- A directional trade can add income by selling an option against it.

Renko Individual Options Combined Into Positions

Orange circle1-Blue circle1: You have an option spread that began as an individual income trade, with the Oct 345 put sold for 4.85.

- Buy the Oct 6 weekly 358 call option for 4.65 when the price envelope reverses.

- Buying the Oct 6 weekly on 9/27 gave the trade 7 trading days to expiration.

- You can combine the long call with the short put to make a synthetic long Renko QQQ position trade = 4.65 – 4.85 = .20 credit.

You can trade the blue circle1 as a long call-short put, which would be the Renko method trade. I am showing 2 individual Renko options trades combined into a single position.

Orange circle 2-Blue circle 2: The price moves to resistance. Sell the Oct 368 call for 4.05 against the QQQ option buy position.

- You bought the 358 calls at 4.85 and sold the 368 calls at 4.05, creating a Renko options position debit spread at .80.

- Price envelope reverse sell. Exit the long call, leaving the short call as an income trade.

- You could also combine your trade with a long put to create a QQQ synthetic short position.

- Buy the Oct 13 357 weekly put at 3.70.

The Renko options combination trade can become a synthetic long with the short call at a credit. Or the long put can become a long debit spread with the short put at a credit.

Again, I am focusing on how individual options trades can become combination position trades. The price envelope reverse sell can be its own long put-short call synthetic short, leaving the short put and short call as Renko option income trades.

Renko Short Option Income Trade Protection

Blue circle 3: I asked the question – What happened to the short Oct 368 call when the Renko QQQ price envelope reverse-triangle breakout buy continued through resistance to a 10/6 daily high of 365.91?

- The higher price move took the short call to a loss. But you combined the short call with a long 360 call to form a debit spread.

- Buy the 360 calls at 3.95 and short the 368 calls at 4.95. You have a long debit spread at a 1.00 cost.

This is a good example of how the Renko option trading position combination protects an individual short option. The price might move higher than 368, and any long calls that are part of this spread will not gain any more profit.

You have protected your short call, and it will not suffer a loss.

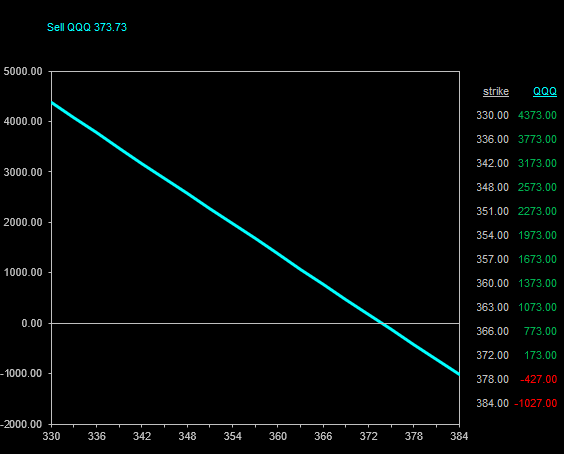

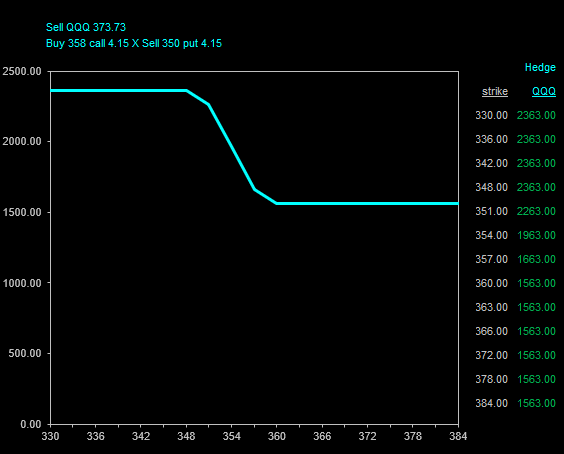

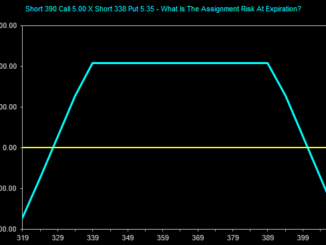

Renko Options Trading And Hedging QQQ Position Trades

Look at the 2 QQQ and Renko options trading profit graphs.

- Graph 1 shows the profit curvature for a short QQQ. You could have created this with options that are at the money: sell a call and buy a put.

- Graph 2 shows the Renko options trading profit curvature for a position hedge.

There is a link below the graphs to a video discussing these graphs and the related QQQ position trades.